Intermodal is Often Cheaper than Truckload, yet Intermodal Sit at ~6% Market Share ... Why?

Here is the number that bothers me about intermodal.

Domestic intermodal accounts for roughly 6% of the 53-foot capacity U.S. freight market. Truckload accounts for 94%.

Truckload capacity is tightening. FMCSA enforcement actions are pulling carriers from the market. Fuel is escalating because of the Iranian conflict. By every traditional signal, this is the environment where intermodal should be taking share. Yet the latest info from IANA’s YTD data shows US intermodal volume down 6.4%.

We just ran a 750-lane study showing intermodal was the more economical option on better than half of spot market lanes analyzed.

So the question is obvious. If intermodal is cheaper on most long-haul lanes, and the savings are real and repeatable, why does 94% of that freight still move on a truck?

Price alone does not explain it. Neither does transit time, though both matter. The real answer has multiple layers. Some are problems the industry can address. Others are structural realities inherent to the mode with no clean solution. Both deserve an honest look.

This article is written to bring those layers into the open.

At the end of this article, you will understand:

How much of the freight market is actually addressable by intermodal, and how much is a structural mismatch

The specific barriers that prevent qualified shippers from converting, from organizational politics to pricing opacity to institutional scar tissue from bad experiences

What the industry, including IMCs and railroads, has done to damage its own cause

What would actually have to change to move intermodal from 6% toward its real potential

The roadmap shippers have successfully used to convert their truckload freight to intermodal where it makes sense

Originally posted on Rick LaGore’s LinkedIn page.

Freight market analysis. Intermodal + truckload. What to do next. Free.

Before the barriers: understanding the market intermodal actually competes in

The 94-6 split looks alarming until you remove the freight intermodal is never going to move.

Short-haul freight dominates the U.S. market. The majority of freight tonnage moves short distances, and that share keeps growing as supply chains regionalize and distribution networks push closer to the end consumer. Freight under 750 miles is functionally unavailable to intermodal. Ramp costs, dray on both ends, container handling: the fixed costs overwhelm any linehaul savings on a short haul. Our lane analysis confirmed this directly. Under 750 truckload is more competitive than intermodal.

That short-haul figure has been growing for twenty-five years, driven by a structural shift. Truckload haul lengths have shortened.

The drivers are well understood. E-commerce pushed distribution center networks closer to population centers, converting long regional replenishment moves into shorter, localized freight. Next-day and same-day delivery expectations reinforced the trend. As the ATA’s chief economist has noted, the continued rise of online sales is forcing supply chains to position inventory closer to the end customer, and that physics works against intermodal’s core strength.

This is the structural backdrop the 94-6 number sits inside. The freight intermodal is best equipped to handle, long hauls above 1,000 miles, represents a shrinking share of total truck volume. In other words, intermodal has not been losing to truckload on a segment of shipments that it is currently designed to compete against.

Strip out the short-haul freight that is not currently addressed, and the real competition is happening in a much narrower lane. Only a relatively small share of U.S. freight is structurally suited for today’s intermodal.

The geography and ramp density problem

The lanes where intermodal delivers strong, repeatable savings are specific corridors between well-positioned ramps. The lanes where it does not work are concentrated in specific regions and distance bands.

This is not a minor asterisk. It is a structural constraint.

The best intermodal economics require an origin within roughly 50-100 miles of a functioning ramp and a destination within the same radius. That sounds manageable until you map actual freight flow origins against ramp locations.

Large portions of U.S. freight originate in secondary and tertiary markets that are poorly served by intermodal ramp infrastructure.

Under Precision Scheduled Railroading (PSR), the Class I railroads knowingly made this worse in their efforts to improve OR (operating ratios). Beginning around 2017 and accelerating through 2021, railroads closed or reduced service at intermodal terminals in dozens of secondary markets in pursuit of efficiency. They optimized for financial metrics at the cost of geographic coverage.

The geography constraint is not solvable by a shipper doing a better analysis.

The service memory problem

The freight industry has a long memory. Sometimes too long.

In 2022, U.S. Class I railroad service quality struggled. Intermodal on-time performance dropped significantly across multiple railroads. Shippers who had built intermodal programs and committed contracted volumes found their freight sitting at ramps, missing appointments, and creating operational chaos downstream.

Before accepting that narrative at face value, two things deserve to be said.

First, intermodal is more than rail. The IMC is the entity ultimately responsible for the intermodal service experience. A well-run IMC controls pickup and delivery through its drayage network and can either absorb what is happening on the rails or make it worse.

The shippers who had the best 2022 intermodal experiences were the ones with IMCs who managed dray proactively, communicated exceptions early, and owned the problem rather than pointing at the railroad. The shippers who had the worst experiences often had providers who did neither, yet continued to tell their customers they can take on more freight.

Second, railroad capacity does not flex like truckload capacity. Adding a truckload carrier can take days. Adding rail capacity takes years of planning and billions in capital investment. Nobody planned for 2022. Nobody could have. The pandemic-driven freight surge was an event with no historical precedent, compressed into a nine-month window, followed by a collapse. Blaming Class I railroads for not having capacity ready for a surge no one saw coming, that would have sat idle for decades after, is not a fair read of what happened.

And truckload had its own struggles in 2022. Two of the three legs of every intermodal shipment involve trucking. The dray capacity problems IMCs faced that year were not railroad problems. They were the same issues as every truckload shipper was dealing with simultaneously, in addition to chassis constraints, and terminal congestion.

While there are a number of astericks, none of that changes what shippers experienced. Service has recovered significantly since then, but the shippers who lived through 2022 did not come back automatically when performance improved. They rebuilt routing guides around truckload. They told procurement teams that intermodal is unreliable. They explained to operations leadership that the extra transit days carry too much risk. That institutional memory is sticky in a way that rate comparisons cannot overcome with a single pitch.

The pushback is simple. You cannot design a rail network around a once-in-a-generation surge any more than you can run a business based on a single anomalous quarter. Dismissing intermodal entirely because of 2022 is not a balanced view. It ignores the structural realities of the network and the meaningful progress made since.

But that is the nature of this mode. Every service failure creates a damage period that lasts years. One bad lane. One missed appointment that cost a plant shutdown. One cycle of demurrage charges on a quarter-end P&L. The shipper who experienced that writes off intermodal for three to five years, sometimes permanently.

Intermodal earns trust slowly and loses it fast. That asymmetry is one of the most underappreciated dynamics in the entire adoption problem.

The pricing opacity problem

This is the one nobody inside the industry likes to talk about. But it is real, and it keeps shippers away from intermodal even when the economics favor it.

A truckload quote is simple. Pickup, delivery, fuel, one invoice. The only variable most shippers deal with is the possibility of detention, and that is a known risk they have learned to manage.

Intermodal is a different conversation. Detention exists with this mode too, but shippers with less operational control over their supply chain can also pick up demurrage, chassis usage, per diem, storage, and ramp congestion charges. These are real costs that can appear on an intermodal invoice with little warning. The savings that looked compelling in the rate comparison disappear in the accessorial reconciliation, and the shipper is left explaining to their CFO why intermodal cost more than expected.

Not all IMCs operate this way. The better providers take on a portion of accessorial risk where it makes sense and actively manage charges to keep them to a minimum. That is the service model intermodal needs more of within its ranks.

But enough of the market operates on a cost-plus, pass-through model that the perception of pricing opacity is both widespread and justified. When that is your first intermodal experience, it is often your last.

The damage shows up in shipper behavior in a specific way. Finance teams remember the quarter intermodal accessorials ate the savings. They add a risk premium to every future evaluation. That premium often tips the analysis back toward truckload even on lanes where a well-managed intermodal program would genuinely deliver what it promises.

The compounding factor is that some of these charges are not anyone’s fault. Chassis availability, demurrage at rail ramps, and dray detention can be driven by terminal congestion, equipment positioning decisions, and railyard operating practices that neither the shipper nor the IMC fully controls. A shipper who does everything right can still get hit. In truckload, that outcome is rare. In intermodal, it is common enough that experienced shippers build it into their expectations before the first quote conversation even starts.

That is the real damage. Not the charges themselves. The anticipation of them.

The drayage problem

Intermodal has three legs. Origin dray. Rail linehaul. Destination dray.

The rail linehaul gets almost all the attention. It is where the structural fuel efficiency advantage lives. It is what the math is built around.

Dray gets almost none of the attention. And it is where intermodal often fails.

Based on direct experience managing intermodal programs, approximately 95% of service failures occur in the dray segment, not the rail segment. Missing a ramp cut-time. Chassis availability issues in certain markets. A dray carrier late on pickup. Destination ramp congestion delaying container availability. These are the moments that define whether a shipper calls intermodal reliable or unreliable, and they have almost nothing to do with the train.

These failures are invisible in most rate comparisons because dray cost and execution risk are modeled at best-case. The quote assumes the container will be picked up on time, the chassis will be available, and the ramp will not be congested. When any of those assumptions breaks, the savings evaporate and the service failure becomes the story the shipper tells internally for the next three years.

The dray market adds structural risk that truckload does not have. Dray carriers are a separate tier of transportation provider operating within limited geographic zones around ramps. Their business model depends on completing multiple short moves per day, since their length of haul is short enough to allow it. But that only works when they are moving. Drayage margins are among the tightest in the freight industry, which means any delay, a missed chassis, a congested ramp, a grounded container that cannot be located, directly cuts into a driver’s ability to earn for the day. That economic pressure creates turnover and capacity fragility that long-haul trucking does not experience in the same way.

And unlike long-haul truckload, where a shipper with enough volume can command priority service, dray carriers at major terminals often operate on allocation or first-come-first-served models that limit shipper control regardless of relationship or volume.

The three-leg structure is intermodal’s fundamental execution challenge. The rail can run perfectly and the shipment can still fail. Until all three legs perform consistently, savings in the linehaul will be partially consumed by cost and variability in the dray segments. The shipper who experiences a smooth rail move and then waits three days to get their container out of a congested destination ramp does not come away with a positive view of the mode.

They come away with a story about why intermodal does not work.

And that story spreads.

The organizational inertia problem

This is the barrier that nobody publishes a data point on, yet it is very much part of the equation.

Inside many shipper organizations, the transportation team is not incentivized to optimize across modes. They are incentivized to cover loads first and manage cost second. No shipper wants stockouts on their sheet. Empty retail shelves mean lost sales, and lost sales can mean lost planogram space that took years to earn. That risk lives in the transportation planner’s mind on every load decision, even when the freight has nothing to do with retail replenishment.

A truck call takes five minutes. Load board quote, carrier who knows the lane, rate agreed in real time, pickup confirmed. Done.

An intermodal conversion takes planning. Lane analysis against ramp locations. Blocking and bracing evaluation. Coordination with operations on cut-times and slightly longer transit. Setting expectations with customer service on delivery windows. TMS configuration for intermodal-specific tracking. An approval process if the mode is new to the organization.

In an environment where a transportation planner is measured on load coverage and on-time delivery, “just put it on a truck” is the safest career decision available. The savings from modal conversion flow to the CFO’s P&L, distributed and invisible in most internal reporting systems. The missed appointment from the one intermodal load that failed gets tied directly to the person who booked it. Specific. Attributable. Remembered.

That asymmetry between upside and downside strongly favors the status quo every single time.

This is why successful intermodal adoption almost always originates with senior procurement leadership carrying an explicit modal diversification mandate. The shipper organizations that have built durable intermodal programs did so because a VP of Supply Chain or a CFO made it a strategic directive, not because a dispatcher decided to try something new on a Tuesday morning.

Without that top-down mandate, the organizational default is always truck. Not because truck is better. Because truck is safer for the person making the decision.

Another part of the inertia may be a quiet feedback loop. Shippers watch the market share data. They see that intermodal’s slice has not grown meaningfully in years. Recent data shows it shrinking. And they draw a conclusion that feels logical even if it is wrong: if the mode were really that good, more people would be using it. Since they are not, maybe there is a reason. So the shipper does not look further, the number stays flat, and that becomes the next piece of evidence for the next shipper who runs the same math.

That loop is self-reinforcing and largely invisible. It has nothing to do with rates, transit times, or corridor economics. It is herd mentality, and it is suppressing adoption on lanes where intermodal would perform well.

The volume requirement problem

Contract intermodal, where the pricing and capacity commitments that make intermodal programs truly work, typically requires a minimum volume commitment. The standard threshold is often cited as three or more loads per week on a lane to justify contracted rates and dedicated capacity.

This requirement is invisible in most rate comparisons, which are done on a per-load basis. A shipper who ships two loads a week on a qualifying lane sees an attractive rate comparison, commits to intermodal, and then discovers that the contracted economics do not apply to their volume level.

Mid-market shippers are particularly affected. The companies running 500 to 2,000 truckload shipments per year, with freight spread across dozens of origin-destination pairs, often cannot concentrate enough volume on individual lanes to qualify for the rates that make the intermodal financial case compelling. Their freight is too fragmented to build consistent intermodal programs, even when their long-haul lanes by mileage would qualify.

The spot market fills this gap partially, but spot intermodal lacks the predictability and priority that makes intermodal operationally reliable for many shippers.

Shippers who most need intermodal as a cost tool, mid-market companies without negotiating leverage in the truckload market, face barriers to accessing the intermodal economics that would benefit them most.

The IMC quality problem

There are roughly 500,000 for-hire carriers and about 700,000 total motor carriers in the United States, along with approximately 25,000 freight brokers.

By comparison, the number of companies that focus on door-to-door domestic intermodal as a core offering is a small fraction of that, likely in the hundreds rather than the thousands. Within that group, the market is concentrated, with the top ten IMCs controlling better than half the market share.

Digging deeper, an even smaller subset of IMCs holds direct ramp-to-ramp contracts with all Class I railroads. The rest access intermodal capacity through door programs or intermediaries that do. The operational difference between these models is significant and largely invisible to a shipper comparing quotes.

A true IMC with direct Class I contracts owns the rate relationship, has priority access to equipment, and can escalate service issues directly with the railroad. An entity accessing intermodal through a door program is effectively a broker, with no direct railroad relationship and limited ability to resolve problems when they occur.

A meaningful portion of the market promotes “intermodal” without operating as true IMCs. This contributes to confusion and inconsistent service expectations. Shippers who believe they hired an IMC but receive broker-level service often have no way to determine whether the issue was the provider model or the mode itself. When service breaks down and the response becomes fragmented across multiple parties with no direct railroad accountability, the conclusion is often that intermodal does not work.

The quality gap within the IMC market remains one of the industry’s most underaddressed problems. It directly suppresses adoption, as negative experiences tend to carry more weight and influence future transportation decisions within shipper organizations.

The freight qualification problem

Not all freight that moves on long-haul truck can move on intermodal. This is understood in general terms, but the specifics are not always communicated clearly, and the consequences of getting it wrong are severe.

Weight restrictions. Intermodal containers carry 2,500 pounds less than a standard over-the-road trailer due to the weight of the container and chassis combination. Shippers who regularly maximize truckload weight often cannot move the same load by rail.

Blocking and bracing requirements. Freight on rail experiences different forces than freight on a truck. Harmonic vibration during rail movement requires proper blocking and bracing to prevent load shifting. Shippers who skip this step discover the problem at the destination, and the product damage becomes the story that circulates internally.

Commodity restrictions. Class I railroads publish prohibited and restricted commodity lists. Certain chemicals, hazardous materials, and high-value goods either cannot move by rail or require special handling that adds cost and complexity.

Temperature control limitations. True temperature-controlled intermodal capacity is more limited than refrigerated truckload capacity, and the performance envelope is narrower. Shippers who need precise temperature control for perishables or pharmaceuticals face a smaller intermodal option set.

Each of these disqualifiers removes freight from the addressable market. And each one represents a category of shipper who tried intermodal, encountered the limitation, and built a rule into their routing guide: this freight type does not go on intermodal. The rule is sometimes applied correctly and sometimes applied far more broadly than the limitation warrants, but once the rule exists it shapes freight decisions for years.

The cycle-chasing problem

Watch how intermodal adoption moves across freight market cycles and you see a persistent pattern.

Truckload capacity tightens. Rates spike. Tender rejections rise. Shippers scramble to find alternatives. Intermodal gets a look. Shippers who had dismissed it start calling IMCs. Short-term programs get set up. Savings materialize.

Truckload capacity loosens. Rates fall. Every load covers easily. The urgency around intermodal evaporates. The programs get quietly discontinued. The operational knowledge built over the tight-market period disperses. The people who learned how to run intermodal move on or shift focus.

The next cycle starts. The scramble repeats.

This is not a theoretical pattern. It has played out in 2018-2019, in 2020-2022, and it is playing out again in 2026. Intermodal gets discovered during capacity crunches and abandoned during soft markets.

The problem is that the best intermodal economics come from consistent programs, not crisis response. A shipper with a well-established intermodal program, contracted capacity, trained operations staff, and integrated TMS visibility performs fundamentally differently than a shipper standing up intermodal for the first time during a capacity squeeze.

Cycle-chasing produces exactly the wrong economics. Emergency intermodal during a tight market means spot rates, limited equipment availability, reduced service priority, and a first-time operations team learning under pressure. The result is often a poor experience that reinforces the narrative that intermodal does not work.

The shippers who successfully use intermodal as a strategic cost tool build programs during soft markets, when time and capacity allow deliberate implementation, and hold them through tight markets, when the savings accelerate and the trucking alternatives become unreliable. Those shippers represent the 6% who have figured this out. The 94% are still chasing cycles.

The knowledge gap

There is a straightforward dimension to the adoption problem that underlies all of the more complex barriers above.

A significant portion of U.S. shippers, particularly in the mid-market, do not have deep operational knowledge of intermodal. They know it exists. They know it involves trains. They have heard it is cheaper on long lanes. But they do not know how to evaluate whether their freight qualifies, how to find a competent IMC, how to handle blocking and bracing, how to integrate intermodal tracking into their TMS, or how to explain the mode shift to their customers and operations teams.

Some of the misconceptions go further than that. Shippers still tell us they cannot use intermodal because they do not operate out of a rail-sided building. Others believe they can only use 53-foot equipment and assume that disqualifies them. Others think they need an onsite lift to handle the containers. None of those things are true, but they are repeated often enough that they function as real barriers. A shipper who believes they are structurally disqualified never asks the next question.

Intermodal has a learning curve that truckload does not. A shipper can book truckload with no prior knowledge of the mode. Intermodal requires operational preparation that is not intuitive and is not documented in any accessible, practical form that most mid-market shippers can easily find and act on.

IANA, Intermodal Association of North America, has worked to address this through education and certification efforts. Individual IMCs, including InTek, publish content designed to walk shippers through the evaluation and implementation process. But the information gap remains wide relative to the scale of the opportunity.

The result is a market where shippers who are theoretically positioned to benefit from intermodal remain on truck because they do not know enough to make the change confidently, and the consequences of a botched implementation feel riskier than the savings feel valuable.

What would actually change the number?

Intermodal’s share within its core long-haul lane set has been relatively stable in recent years, with incremental gains during tight capacity cycles like the pandemic, followed by normalization. The bigger question is what it would take to materially increase that share over time.

Some of it requires industry action that individual shippers cannot drive.

Rail service has to stay reliable. The 2022 service collapse and the PSR-related ramp closures of the previous decade created damage that is still being recovered from. Railroads that continue to optimize for operating ratio at the expense of geographic coverage and service consistency are actively limiting intermodal’s market potential. On-time performance has significantly improved since 2022, but shippers need to see the published service levels to be consistently reliable and they need to understand the challenges we discussed earlier in this article as to what happened in 2022.

The dray execution gap has to close. The mode will not penetrate deeper into the shipper market until the dray execution standard comes closer to what shippers experience from well-run truckload carriers.

Pricing transparency has to improve. The portion of the IMC market that operates on linehaul-plus-pass-through without accessorial accountability is actively damaging adoption. Negative surprises get attributed to the mode, not the pricing model, and that is a distinction shippers do not make after the first bad invoice.

The fix is not complicated. If a cost is predictable and recurring on a lane, build it into the price. Yes, the all-in number will not show 20%-plus savings against truckload. But a quote that saves 10% and delivers exactly what it promised wins the business and keeps it. A quote that shows 30% and lands at 12% after accessorials loses the business permanently and sends another shipper back to truck with a story to tell.

Transparent pricing that slightly underwhelms on paper beats opaque pricing that dramatically disappoints in execution. Every time.

The IMC quality standard needs teeth. The industry’s inability to clearly differentiate between true IMCs and entities using door programs creates information asymmetry that harms shippers and suppresses adoption. An IANA-governed certification with meaningful standards, similar to the UIIA framework, would help shippers identify providers with direct railroad contracts and accountable service models. This conversation is overdue.

Build programs during soft markets. The shippers that have figured out how to build their programs when there was time and capacity to implement them well have a leg up on other shippers. Now, with intermodal pricing at or near cycle lows and truckload tightening, is exactly the right time to run the lane analysis, qualify the freight, find a competent IMC, and build the operational muscle before the next capacity crunch makes everyone scramble.

Evaluate the full landed cost. Not the linehaul rate. The door-to-door rate including dray, fuel surcharge, and expected accessorials. If your IMC cannot or will not quote all-in, that is a provider problem to address, not a mode problem to dismiss.

Start with the right lanes. The freight that has never worked in intermodal will never work in intermodal. The qualifying long-haul freight where the mode is structurally competitive is a large absolute number. Most shippers have at least some lanes in that universe. The analysis to find them is not difficult. The decision not to do it is.

Treat intermodal as a strategic platform, not a spot option. The companies getting the most value from intermodal use it as a core element of their long-haul transportation strategy, not as an emergency overflow when trucks get expensive. That means contracted capacity, consistent volumes, and operational integration, not one-off spot loads during a capacity squeeze.

When intermodal actually works: the four conditions that have to be true simultaneously

The previous sections documented what holds intermodal back. This section is the other side of that ledger.

Intermodal works when four conditions are true at the same time. Not three. All four. When any one of them is absent, the economics or execution begin to break down.

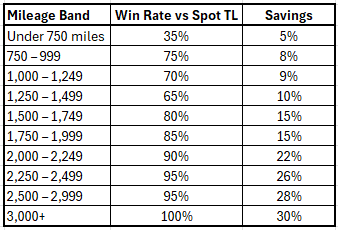

Condition 1: The lane is long enough.

The data from our 750-lane February 2026 analysis is clear on this. Above 1,500 miles, intermodal wins 82% of spot lanes. Above 2,000 miles, the win rate is 93%. Below 750 miles, intermodal is often not the choice when compared against truckload.

The practical floor is somewhere between 700 and 800 miles depending on the specific corridor. The acceleration above 1,500 miles is not marginal. Savings nearly double when you cross that threshold, and the win rate jumps 16 percentage points. That jump is structural, not cyclical.

Condition 2: The corridor is structurally supported.

Two lanes of identical distance can produce very different intermodal results depending on origin and destination market structure. The residual data in our analysis, which measures how much a state or corridor over- or underperforms the expected savings for its distance, shows this clearly.

The corridors that work have ramp density, carrier competition, and freight flow orientation that compound the rail economics. The corridors that do not work have structural headwinds, usually from port market premium pricing, abundant regional truckload capacity, or limited ramp access, that eat into the linehaul savings before they reach the shipper’s invoice.

Condition 3: The freight qualifies.

Intermodal cannot move everything. Weight-sensitive freight, time-definite shipments with no transit buffer, certain commodities with railroad restrictions, and freight requiring specialized equipment that is not available in 53-foot domestic containers are all outside the intermodal universe.

The blocking and bracing requirement deserves specific mention because it is the operational detail most new intermodal shippers miss. Rail movement creates harmonic vibration that standard truckload packing does not account for. Shippers who load a container exactly as they would load a trailer often experience product damage on the first few loads. The fix is not complicated, typically staggered pallet patterns plus a simple 2x4 footer to secure the last row, but it requires awareness and process adjustment that takes time to implement correctly.

Condition 4: The shipper has the operational readiness to execute.

Intermodal requires planning that truckload does not. Cut-times at ramps are fixed and unforgiving. Transit windows need to be communicated to operations and customer service teams. Blocking and bracing standards need to be embedded in the loading process. TMS visibility for rail tracking needs to be configured differently than truckload tracking. And the IMC relationship needs to be managed as a partnership, not a transaction.

Shippers who treat intermodal as a drop-in truckload substitute discover that the mode requires deliberate operational integration to perform consistently. The companies that have built successful intermodal programs did not do it by making calls on Mondays and hoping for the best. They built processes, trained teams, and treated the first 90 days as a setup period, not a performance period.

When all four of these conditions are in place, the economics and service excel.

What shippers should do right now

The data in this analysis points to a specific set of actions for shippers who have qualifying freight. None of them require waiting for the industry to solve its structural problems.

Run the lane analysis before the next freight cycle tightens.

The current market is one of the best environments in recent memory for building an intermodal program. Intermodal pricing is at or near cycle lows. Equipment availability is strong. Rail service has stabilized. Truckload capacity is tightening from supply attrition rather than demand growth, and that dynamic makes the rate spread wider today than it typically is.

The shippers who act in soft markets build better programs than the shippers who act in tight markets. They get deliberate onboarding instead of emergency coverage. They get contracted rates instead of spot premiums. They get 90 days to train their operations teams instead of 90 minutes to cover a load.

Identify your lanes above 1,500 miles. Match them against the corridor data. Pull quotes that include all-in landed cost, not linehaul only. That analysis takes days, not months. The results will show you where your money is sitting on the table.

Start with the structural corridors, not the marginal ones.

The transcontinental corridors in this dataset where the economics are undeniable and the structural support is proven. Start there. Build the operational confidence and the provider relationship on lanes where you have maximum margin for error because the savings are large enough to absorb imperfection during implementation.

Once those lanes are running cleanly, expand to the corridors where the economics are strong but slightly more sensitive: mid-haul lanes in the 750-1,499 mile range where corridor and state residuals are positive.

Pick the right IMC, not just the cheapest quote.

The difference between a true IMC with direct Class I railroad contracts and an entity using a door program is invisible in the rate quote and visible in the service delivery. Ask directly: do you hold direct intermodal contracts with all Class I railroads? Ask for documentation. The answer determines whether your IMC can actually escalate and resolve service issues with the railroad when something goes wrong, or whether they are as dependent on the railroad’s goodwill as you are.

Treat the first 90 days as an investment, not a performance test.

The first quarter of a new intermodal program is when blocking and bracing processes get refined, when cut-time compliance gets built into scheduling, when the operations team learns what intermodal tracking looks like versus truckload tracking, and when the IMC relationship gets tested and calibrated. Shippers who treat the first 90 days as a pilot with a high pass/fail bar often kill programs that would have worked once the operational kinks were resolved.

Define what success looks like before the first load moves. Set realistic service expectations for transit, typically one to two days longer than truckload on comparable lanes. Measure landed cost including all accessorials, not just base rate. Give the program time to mature before drawing conclusions.

The close: competitive advantage goes to whoever acts first

Intermodal is at 6% of the long-haul freight market. The economics in this analysis say it should be significantly higher. The gap between those two numbers is not explained by transit time alone.

It is explained by two decades of service failures and recovery, by pricing models that buried savings in accessorial surprises, by organizational incentive structures that punish the person who booked the failed load and invisibly reward the person who kept freight on truck, by ramp closures that removed viable intermodal options from entire regions, and by a provider market that blurs the line between true IMCs and brokers wearing IMC labels.

None of those barriers are permanent. Some are already being addressed. Rail service is better today than it was in 2022. The conversation about IMC certification is happening at the IANA level. Several Class I railroads are adding intermodal schedules and improving terminal access in underserved markets.

But the improvement is gradual and the opportunity is now. Intermodal pricing near cycle lows. Truckload tightening from supply attrition. A rate spread between modes at one of its widest points in recent memory.

The companies that build intermodal programs now, on the right lanes, with the right providers, and with the operational integration to execute consistently, will carry a structural freight cost advantage into the next cycle that their competitors will not have. When truckload tightens fully and spot rates continue climbing, those companies will not be scrambling to find intermodal capacity on emergency terms. They will already have contracted capacity, trained operations, and proven lanes.

The window is open. The data tells you exactly where to look. The only remaining question is whether your organization treats this as a freight market moment or as a strategic infrastructure decision.

The 6% who have figured intermodal out made the second choice. The 94% are still choosing the first.

Want to go deeper on intermodal?

Visit InTek Logistics, read our blog, check the InTek Intermodal Index for weekly rate updates, and listen to the InTek Intermodal Podcast.

Rick LaGore CEO, InTek Logistics